The Skinny on Tallboys

Have you ever polished off a pint of your favorite year-round beer and thought, I couldn’t possibly drink three more ounces…? Unlikely, yet when it comes to the increasingly popular 19.2oz can in craft beer, that extra volume changes the entire competitive landscape. Also known as “tallboys”, 19.2oz cans present significant barriers to entry compared to traditional formats, including volume requirements, equipment compatibility, distribution muscle, and the retailer relationships. There’s a common assumption that the format is just a flash-in-the-pan gimmick having a cup of coffee in the craft beer space, but that couldn’t be further from the truth. Tallboys are a new weapon in the category’s evolution, infiltrating one of the last frontiers at retail: Convenience. The format however isn’t a good fit for everyone, in fact, it doesn’t make sense for most breweries at the moment. Here’s the skinny on tallboys:

A few months ago, I stopped by Capone’s Liquor, a popular bottle shop that also serves as a convenience store to Chicago’s Avondale neighborhood. As I was chatting with their buyer Marc, a man walked up to the counter with a bag of chips and an Anti-Hero 19.2oz can. The newest format for our best selling beer had been performing great, but I never get to see who is actually buying them. I told the man that I worked at the brewery and appreciated the support, then followed by asking what he likes about that format. The man was confused by why I would even need to ask the question and replied, “Where I’m heading, I only need one.”

Retailers

Convenience stores are where you’ll find tallboys in abundance. Located at busy intersections, near train stations, and at highway exits, their customers are looking for short term needs, not to stock their refrigerator. They’re willing to pay a higher price per ounce for only one can, a premium for convenience. Stores include the likes of not only 7-Eleven as an example, but also drug stores like Walgreens & CVS, and gas stations. While these outlets face competition from small, independent stores like Capone’s, the majority of the volume travels through chains.

As convenience becomes of growing importance to the purchasing mindset, grocery stores are becoming bigger players in the single-serve format as well. Nielsen reported last year that 46% of consumers view shopping as a chore and that “consumers are replacing stock-up grocery shopping trips with smaller, more frequent needs-based trips.” In Chicago, I’ve been noticing the shift with my own eyes as my local neighborhood grocery stores, as well as the larger chains, are shifting their cooler space around to offer more single-serve cans, both craft and macro brands.

Each time I visit my in-laws in Sacramento, CA, I visit their local Whole Foods only to find a wider display of 19.2s. Three visits ago I grabbed an Anchor Steam, then a Deschutes Fresh Squeezed IPA on my next trip, and this past April I took home Sierra Nevada’s Hazy Little Thing, all 19.2oz cans for about 3 bucks. I’d had each beer before, just not in awhile, and was happy to revisit them without committing to an entire six-pack. The single can, albeit an oversized one, was perfect. This less talked about advantage of the tallboy is the sampling opportunity, which can lead to increased brand loyalty and stronger performance by the brand’s primary package.

If you ask most craft brewery founders around the country though, their ambitions do not include 19.2oz cans nor diving deep for this wide of a consumer base by taking on such a competitive channel. And that’s a good thing, because they probably couldn’t get there if they wanted to.

Breweries

While low volume, shrink-wrapped can manufacturers are springing up all over the country, there’s only two major players to order printed cans. Of the two, only one even offers 19.2 cans and the order volume is still so tiny compared to 12oz & 16oz that they only produce them 3-4 times per year. To place an order and avoid penalties, you have to purchase a minimum of 25 pallets (126,452 cans). Not only is that a lot of empty cans that will chew up valuable real estate in the brewery, that’s a lot of beer. 612 BBLs to be exact, which is more than a lot of breweries produce in a year. See where I’m going with this?

You can’t have multiple brands counting toward the order minimum either, it needs to be a single brand. Given the tallboy customer, which isn’t typically a beer hobbyist, only strong brand names will have a chance of making a dent in those 126,452 cans. A lot of small, newer breweries don’t even have a lead, flagship brand and instead rely on a vast range of rotating beers to keep customers engaged. Constant rotation will not work in convenience store coolers, not yet at least, leaving these opportunities to the well-established players for now.

With the opportunities at convenience stores being so limited, it takes an impressive selling story to get your beer on the shelf. At these sophisticated companies, that will require a lot of convincing data, which is most commonly available via IRI and Nielsen scan data. If that’s not a space that the brewery is currently winning in, then the convenience door will likely to be closed.

It also takes a pretty high-end filler to be able to adjust the height of the can on the fly, from the brewery’s standard 12 or 16 ounce cans, up to 19.2 ounces. In a lot of cases, it’s not even an option, and in others, the amount of mechanical adjustments is not worth the effort to change right back the next day. The new high-tech fillers have the ability to “change over” (in height) more quickly, but again, the breweries who can afford that type of capital investment are typically limited to the larger, more sophisticated breweries in your region.

Distribution

Let’s say that the brewery is able to get past the volume, flagship, data, and equipment hurdles mentioned. They still need to be partnered up with a powerful distribution network who can get you deep in these chains, which typically requires being aligned with the largest distributors. Why?

Level of Service - The Bud/Miller/Coors distributors have existing relationships and track records with these chains and are already stopping there weekly, or more. High volume accounts, especially with limited space like convenience, require frequent deliveries that a boutique distributor or self-distributing brewery isn’t equipped to service consistently, in most cases. It’s also more difficult for a small local brewery to gain the trust of a regional chain buyer when it comes to remaining in stock and avoiding supply hiccups. The smaller the brewery, the less likely they have the backstock to ensure the shelves never run dry.

Reach - Buying decisions for convenience chains used to be made nationally, meaning that if your distribution reach didn’t cover all locations, you’d never get on the shelf. As craft gained steam over the last decade, geography constraints have loosened and the buying became more regional in order to offer better variety. Now, regions may be divided into smaller zones to allow for local options. Even within a zone which can still stretch a wide distance, a lot of small breweries would struggle to adequately cover the entire area. Since the majority of the beer sold in convenience locations is outside the definition of craft, the big distributors are in a better position, volume-wise, to make stopping at each location a profitable and reliable venture.

The Data (19 - 24oz single serve cans)

I haven’t been including a lot of data in my posts this year because it doubles the amount of time it takes to get a post up. That being said, I wanted to dig into tall cans and make sure my suspicions were accurate. Given that Winter is Here in the beer industry right now, the following trends are very refreshing, especially for craft, and should show you why I love this topic:

Craft Only - Single Serve cans have been growing at a torrid pace in craft, and continue to slay even in this tough market. From 2017 to 2018, craft tallboys grew from $9.5MM to $39.8MM in sales at IRI tracked locations +322%. Let’s get current though. Year-to-date in 2019 (through ~May), compared to the same time period in 2018, they are up an additional $14.5MM, which is +164% through the first 5 months of the year. In dollars, 2019 looks like it will outpace 2018’s growth. Giddy up.

All Beer - When considering all beer, both craft and macro, 19-24oz cans grew $107.2MM in 2018, +10%, of which 28% was made up of craft. Through May of 2019, tallboys continue to be +10% over 2018, but this year 33% of the $ growth is craft.

Here’s a summary of craft’s overall share in the category over the last couple years:

Note: YTD Numbers are approximately through May 19th, 2019

So in the last 18 months, craft has gone from .85% of the total pie to 4.97%. Golf clap.

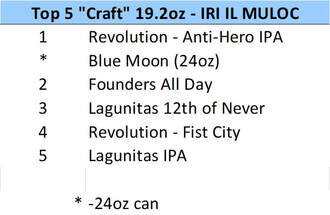

Here’s a snapshot of who the biggest players are nationally and in my home state of Illinois. Am I just sneaking in some Anti-Hero and Fist City love? Perhaps, but honestly I get bored reading about IRI data when only talking about the US as a whole, because it’s hard for anyone to crack the leaderboards dominated by Boston Beer/Sierra/New Belgium due to their size & reach. Any IPA they release is going to be one of the best selling IPAs nationally. Digging in locally is more fun and relevant personally, but it limits the audience for the material, so I get it. Regardless, here are the top five 19.2oz cans in the US and Illinois respectively, thus far in 2019:

Wrap Up

Beer writers, content creators, and beer enthusiasts are not the target demographic for single serve cans, so their presence can barely be felt on social media. The fact that tallboys aren’t popping up in your newsfeeds though does not mean they’re not seeing success. They’re on absolute fire, aligning perfectly with trends in consumer shopping habits. Commuters love them for long daily journeys from the city back to the suburbs, especially on a Friday, or on the way into town for a game or concert. And like Vin Diesel said in The Fast and the Furious, some live their life 19.2 ounces at a time. Or something like that.

So should you expect to find tallboys at your local taproom any time soon, where convenience is not a common selling story? I suspect we actually will start seeing stickered 19.2 cans or the pricey shrink-wrapped can option being attempted by breweries here and there. I'm sure there's already been a handful. Will that be a new frontier for local craft, whether direct-to-consumer or through small independent stores? I wouldn’t bet on it, but I wouldn't bet against it either. I would however bet on tall cans continuing to gain space in both convenience and other less traditional outlets, with craft continuing to eat into the pie and overindex on the growth for a couple more years. The margins may not be thick, but the volume enables a brand to reach new heights.